- Ena Source Monthly Newsletter

- Posts

- Monthly Supply Chain Pulse - 20

Monthly Supply Chain Pulse - 20

📰 Supply Chain Pulse | Monthly Edition – July 14, 2025

Your Go-To Source for Supply Chain Insights, Trends, and Actionable Advice

Supply Chain Theme of 2025: Success will be measured by resilience and cost efficiency.

📊 Key Metrics

Staying competitive means keeping an eye on the data that matters most. Here are five supply chain metrics that we monitor and will provide updates on within each newsletter.

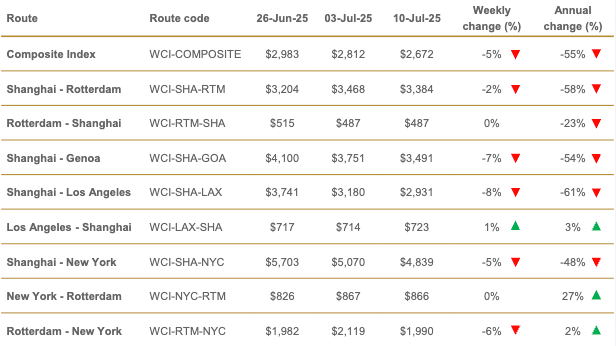

🛳️ Drewry World Container Index (WCI)

Click Chart To See Full Index

The 40ft container shipping rate from Shanghai to New York fell 6.4 % this month, dropping from $5,172 to about $4,839.

Why it matters: After two straight months of sharp increases, a modest pull-back suggests capacity is catching up to demand as carriers add sailings and shippers pause spot bookings now that spring and summer orders have landed.

What to consider: If volumes rebound in late summer, rates could bounce quickly. It is wise to model best and worst case freight costs in your Q3 pricing.

🚚 DAT Truckload Freight Rate Index

Click Chart To See Full Index

The national average Van Spot Rate increased to $2.08 per mile (4% jump).

Why it matters: The slightly increased rate is something that is expected around this time of year as summer shipping is in full swing. We expect to see some relief here in the next few months.

🛢 Commodity Research Bureau (CRB) Index

Click Chart To See Full Index

The CRB index measures a basket of 19 commodities including energy, agriculture, and metals. It’s widely considered a leading indicator of inflation, economic health, and overall cost trends for goods across the market. An increase tends to signify an increase in economic activity while a decrease tends to signify a slowdown in economic activity.

This month, the index rose by 4.5%.

What to consider: Use this data to drive your negotiations with suppliers when reordering or looking for longer term pricing agreements. We highly recommend negotiating 60-90 day price hold agreements where possible.

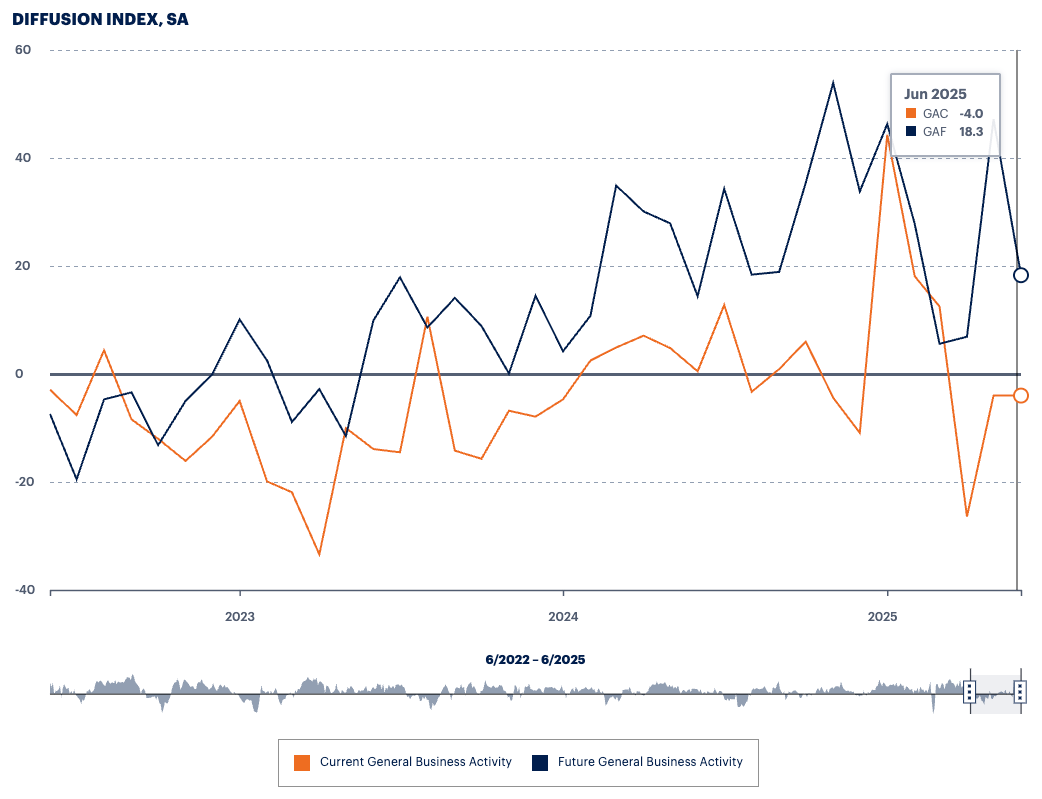

🇺🇸 🏭 Philadelphia Fed Manufacturing Index

Click Chart To See Full Index

To create this index, the Federal Reserve Bank of Philadelphia surveys around 250 manufacturers, asking about factors like employment, working hours, new and unfilled orders, shipments, inventory levels, delivery times, prices, costs, and business forecasts for the next six months. An index level above zero signifies improving conditions, while a level below zero indicates worsening conditions. Read more here.

The diffusion index for current general activity remained unchanged at -4.0 in June.

Why it matters: A flat reading suggests regional manufacturing has found a floor: activity isn’t improving yet, but it has stopped sliding. Stability gives you a clearer baseline for planning production and inventory rather than chasing a falling market.

What to consider: Use this pause to confirm supplier capacity and lead-time commitments before demand picks up. Lock in quotes where possible, and keep safety-stock lean but ready so you can scale quickly if the index turns positive in late summer.

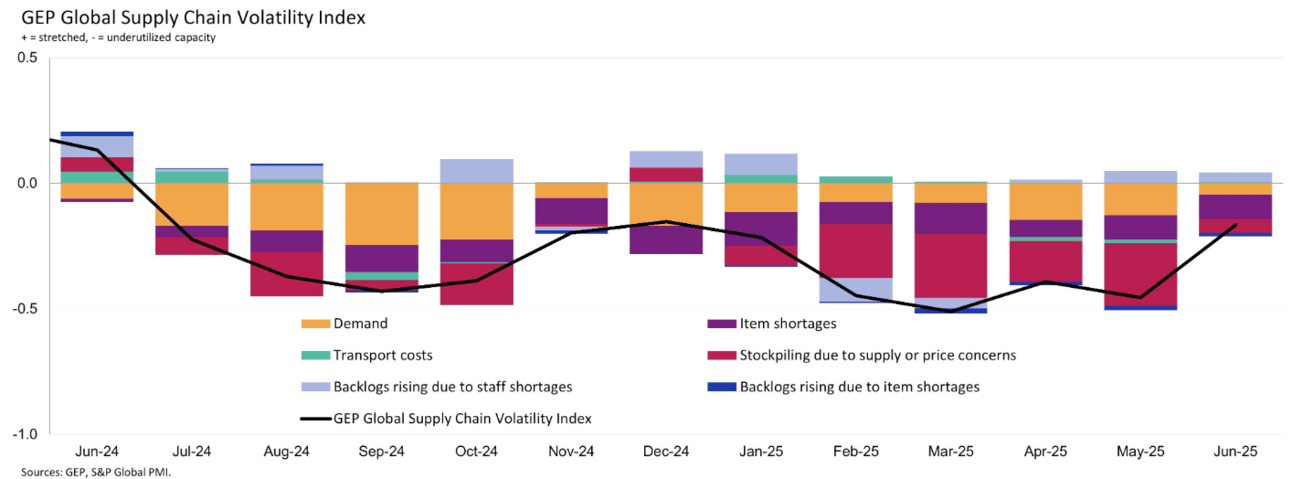

🧾 GEP Global Supply Chain Volatility Index

Click Chart To See Full Index

The GEP Global Supply Chain Volatility Index moved up to -0.17 in June from -0.39 in April. The reading is still below zero, signaling under-used capacity, but the rise shows volatility is creeping back after 12 consecutive months of negative readings.

Why it matters: Capacity is no longer as slack as it was this spring, which means lead-time cushions may start to shrink and freight discounts could taper off. A shift toward zero often precedes tighter transport lanes and quicker price adjustments from suppliers.

What to consider: Use today’s remaining slack to finish price renegotiations and lock in carrier space for Q3–Q4. Revisit dual-sourcing or buffer-stock plans now before the index turns positive and competition for capacity heats up again.

🌍 Global Hot Topic: China and EU Clash Over Critical Rare Earth Controls (Click To Read Article)

On 11 July, the European Parliament formally condemned Beijing’s tightening controls on rare-earth exports; within 24 hours China’s mission to the EU fired back, urging Brussels to “stop politicizing trade” and hinting that restrictions could tighten further. China supplies roughly 60 % of global rare-earth output and 85 % of processing capacity, while the EU relies on it for 98 % of its imports. Prices for neodymium and praseodymium, which are critical for EV motors and wind-turbine magnets, have already jumped 35 % since January, and traders expect more volatility if negotiations stall.

Why It Matters:

A deeper rift over rare earths would ripple far beyond Europe: higher magnet and micro-component prices flow straight into the cost of electric vehicles, wind turbines, smartphones, and defense electronics. If export quotas tighten further, manufacturers worldwide could face sudden margin pressure, production delays, or costly product redesigns just as clean-energy demand is accelerating.

🇺🇸 US Hot Topic: 30% tariffs on EU and Mexico (Click To Read Article)

On 12 July President Trump issued formal notices to Brussels and Mexico City stating that every product entering the United States from the European Union or Mexico will face a 30 % tariff starting 1 August 2025 unless new trade deals are signed beforehand. The surcharge is on top of existing sector duties—50 % on steel and aluminum and 25 % on autos—which will remain unchanged. Similar letters with rates from 20 % to 50 % have reportedly gone to 23 other trading partners, but the EU and Mexico are by far the largest targets: together they account for nearly 22 % of total U.S. goods imports, from automotive parts and machinery to produce, wine, and specialty chemicals.

Why It Matters:

A flat 30 % duty on such a broad range of goods would hit U.S. manufacturers and distributors long before it dents foreign exporters. Auto, HVAC, food-processing, and electronics firms that lean on European precision parts or Mexican wire harnesses, castings, and produce would see immediate cost spikes, squeezed margins, and potential component shortages as suppliers renegotiate.

Ena Source’s stance is simple: don’t wait for diplomacy to solve this. We are already shifting clients to our network of U.S. machining, rubber-molding, and metals partners to lock in competitive domestic pricing before demand floods in. Acting now can blunt most of the tariff shock; waiting a few months could leave businesses scrambling for capacity that’s no longer available.

📈 Ena Monthly Stock Pick

$AMD – A leader in high-performance CPUs, GPUs, and adaptive computing, Advanced Micro Devices is emerging as one of the most credible challengers to NVIDIA in the fast-growing AI and data-center market. The recent launch of its MI300 accelerator platform and the first wave of cloud-provider design adds a powerful new revenue stream alongside its Ryzen PC chips, EPYC server processors, and Xilinx adaptive-logic portfolio. AMD’s total addressable market is expanding by tens of billions of dollars. Profit margins have begun to rebound as the PC slump eases, and management expects double-digit revenue growth in the second half of 2025.

As always, it’s not about timing the market, it’s about time in the market

Disclaimer: This is not financial advice or a recommendation for any investment. The content is for information purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice.

🚀 Your Supply Chain, Your Competitive Edge

Supply chains aren’t just about logistics, they’re about your bottom line, your growth, and your ability to outpace the competition. At Ena Source, we don’t just find suppliers; we engineer strategic supply chain solutions that cut costs, build resilience, improve reliability, and free up your cash flow.

If you’re curious how much you could be saving, let’s talk. No pressure. No cost. Just clarity.

📩 Click here to book a meeting. Resilient supply chains don’t happen by chance, they happen by choice. Let’s build yours, strategically.

Check Out Previous Newsletters At Our Website!